May this holiday season bring you love, joy, and hope.

Article Courtesy of Keeping Current Matters / The KCM Blog

But what many people don’t realize is that even in today’s market where there are more buyers than homes for sale, there are still things that can cause delays or even keep a house from selling. According to Zillow, in 2024, as many as 1 in 3 sellers took their home off the market before it ultimately sold.

And while the reasons those houses didn’t sell are going to vary, there are some general themes that come through. If you’re having trouble getting your house sold, here are the top three hurdles that could be getting in the way, and how an expert agent can help you solve these issues.

It’s no surprise that price plays a major role when you sell. And in today’s market, overpricing a home in a high-mortgage rate environment is the biggest thing keeping homes on the market longer than the norm. As. U.S. News Real Estate says:

“Talk to any real estate expert, and the first thing they’ll tell you is that a house is selling slowly because the price is too high.”

While it’s tempting to push the price higher to get more for your home, overpricing can really turn away potential buyers. It can also make your house sit on the market for far too long. And the longer it sits, the more skeptical buyers will be that there’s something wrong, even if there isn’t.

Not to mention, buyers today have so many tools and resources to view homes in your area and compare prices. So, if your house is priced too high, you’ll risk driving away potential offers.

To find out if this is happening with your listing, talk to your agent about what they’re hearing at open houses and showings. If the feedback is consistent, it may be time to re-evaluate your asking price.

You only get one chance to make a great first impression on a buyer. That’s why sprucing up your house can be the difference between it selling or sitting.

First, take into account your home’s curb appeal. There may be easy ways you can clean up the landscaping to make it tidy, inviting, and really make an impact. As an article from Realtor.com notes:

” . . . for better or worse, buyers do tend to judge a book by its cover. You want to make sure potential buyers’ first impression of your home is a good one—and inspires them to stop by the open house or schedule a tour—so they can see more.”

But don’t stop at the front door. Small touches like removing personal items, reducing clutter, and cleaning the floors give buyers more freedom to picture themselves in the home. And inexpensive upgrades like a fresh coat of paint or updated listing photos to match the current season can go a long way with that wow factor.

When in doubt, lean on your real estate agent for expert advice and whether you need a new game plan to close the deal.

Another big mistake you can make as a seller is limiting the days and times that buyers can view your house. Because at the end of the day, if buyers can’t take a look around, your chances of selling decline — drastically.

And here’s something else to consider. No matter what type of market you’re dealing with, buyers from outside the area are often highly motivated, but they don’t have as much flexibility or time as those who are local. So, give your house the best visibility by making it available as much as possible.

Happy Thanksgiving

With grateful appreciation to all who have served our country.

|

| Beautiful tribute to our Veterans by Richard Kerry Thompson. YOU RAISE ME UP |

SEMPER FI

|

| My husband and his Basic School brothers gathered at the Vietnam Veterans Memorial. |

Article Courtesy of Keeping Current Matters / The KCM Blog

“ . . . now is the time to start thinking about what you need for your next home and then taking those steps to prepare to list . . . We have survey data that says 47 percent of sellers are taking longer than a month to get their home ready to sell, so getting them to start that process early can mean more flexibility.”

By starting your prep work early, you’ll give yourself plenty of time to get your house market-ready by the end of the year. But be sure to partner with a great agent before you get started, so you have expert insight into what repairs are worth it based on your local market.

To get the best price and sell quickly, it’s important that your home looks its best. And that means it’s up to you to make the necessary repairs, declutter, and even consider updates that could add value as part of getting your house ready to list.

By starting now, you can tackle things one task at a time. Whether it’s fixing that leaky faucet, refreshing your landscaping, or painting a room, getting an early start gives you the flexibility to do the job right and with as little stress as possible. Because, if you wait to knock items off your list later on, they could quickly stack up and get overwhelming. As Realtor.com explains:

“There are some important repairs to make before selling a house, so don’t be in too much of a hurry to get your home listed … if you move too fast, buyers see right through the fact that you skipped important home renovations. And this . . . might end up costing you time and money.”

Feeling motivated to start chipping away at that to-do list, but not sure where to start? Here’s a look at the most common improvements other sellers are making today (see graph below):

And while that data gives you a starting point, it shouldn’t be seen as a comprehensive list. What buyers want in your area may be different, and only a local agent will have this in-depth understanding.

For example, if homes in your area are selling quickly with updated kitchens, your agent might suggest focusing on minor kitchen improvements rather than spending money on other areas that won’t offer as much return. They’ll also help you figure out if tackling larger projects, such as replacing your roof or upgrading your HVAC system, is worth it based on other recently sold homes. As Point says:

“Not all renovations are created equal, and focusing on upgrades that offer the highest potential for increasing your home’s value is key.”

And remember, it’s not just big-ticket items that can have an impact. Your agent will also speak to some of the smaller details – like cleaning up your yard, adding fresh mulch, or painting your front door – to make a real difference in how buyers feel about your home. This type of expert eye is crucial to help your house sell fast and for top dollar.

Thinking of selling your house next year? Don’t wait until the last minute to get it ready. By getting a head start now, you can ensure everything is in place by the time the new year rolls around.

Need advice on what to tackle first? Connect with a local agent.

Infographic Courtesy of Keeping Current Matters / The KCM Blog

Thinking about making a move in 2025 and wondering what you can expect? Here’s what expert forecasts say lies ahead.

Article Courtesy of Keeping Current Matters / The KCM Blog

“They’re ready to cut, just as long as we don’t get an inflation surprise between now and September, which we won’t.”

But what does this mean for the housing market, and more importantly, for you as a potential homebuyer or seller?

The Federal Funds Rate is one of the key factors that influences mortgage rates – things like the economy, geopolitical uncertainty, and more also have an impact.

When the Fed cuts the Federal Funds Rate, it signals what’s happening in the broader economy, and mortgage rates tend to respond. While a single rate cut might not lead to a dramatic drop in mortgage rates, it could contribute to the gradual decline that’s already happening.

As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), points out:

“Once the Fed kicks off a rate-cutting cycle, we do expect that mortgage rates will move somewhat lower.”

And any upcoming Federal Funds Rate cut likely won’t be a one-time event. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Generally, the rate-cutting cycle is not one-and-done. Six to eight rounds of rate cuts all through 2025 look likely.”

Here’s what experts in the industry project for mortgage rates through 2025. One contributing factor to this ongoing gradual decline is the anticipated cuts from the Fed. The graph below shows the latest forecasts from Fannie Mae, MBA, NAR, and Wells Fargo (see graph below):

For current homeowners, lower mortgage rates could help ease the lock-in effect. That’s where people feel stuck within their current home because today’s rates are higher than what they locked in when they bought their current house.

If the fear of losing your low-rate mortgage and facing higher costs has kept you out of the market, a slight reduction in rates could make selling a bit more attractive again. However, this isn’t expected to bring a flood of sellers to the market, as many homeowners may still be cautious about giving up their existing mortgage rate.

2. It Should Boost Buyer Activity

For potential homebuyers, any drop in mortgage rates will provide a more inviting housing market. Lower mortgage rates can reduce the overall cost of homeownership, making it more feasible for you if you’ve been waiting to make a move.

While a Federal Funds Rate cut is not expected to lead to drastically lower mortgage rates, it will likely contribute to the gradual decrease that’s already happening.

And while the anticipated rate cut represents a positive shift for the future of the housing market, it’s important to consider your options right now. Jacob Channel, Senior Economist at LendingTree, sums it up well:

“Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever. Buy now only if it’s a good idea for you.”

The expected Federal Funds Rate cut, driven by improving inflation and slower job growth, is likely to have a positive, albeit gradual, impact on mortgage rates. That could help unlock opportunities for you. When you’re ready, connect with a local real estate agent so you’re prepared to take action.

It’s important to note that these communities aren’t just for people who need extra support – they can be pretty vibrant, too. Many people who are downsizing opt for this type of home because they’re looking to be surrounded by people in a similar season of life. U.S. News explains:

“The terms ‘55-plus community,’ ‘active adult community,’ ‘lifestyle communities’ and ‘planned communities’ refer to a setting that caters to the needs and preferences of adults over the age of 55. These communities are designed for seniors who are able to care for themselves but may be looking to downsize to a community with others their same age and with similar interests.”

If that sounds like something that may interest you, here’s one thing to consider. You may find you’ve got a growing list of options if you look at this type of community. According to 55places.com, the number of listings tailored for homebuyers in this age group has increased by over 50% compared to last year.

And a bigger pool of options could make your move much less stressful because it’s easier to find something that’s specifically designed to meet your needs.

On top of that, there are other benefits to seeking out this type of home. An article from 55places.com, highlights just a few:

If this sounds appealing to you, reach out to a local real estate agent. They’ll be able to walk you through what’s available in your area and the unique amenities for each community. You may find a 55+ home is exactly what you’ve been searching for.

-------------------

Article Courtesy of Keeping Current Matters/The KCM Blog

Looking ahead to 2025, it’s important to know what experts are projecting for the housing market. And whether you’re thinking of buying or selling a home next year, having a clear picture of what they’re calling for can help you make the best possible decision for your homeownership plans.

Here’s an early look at the most recent projections on mortgage rates, home sales, and prices for 2025.

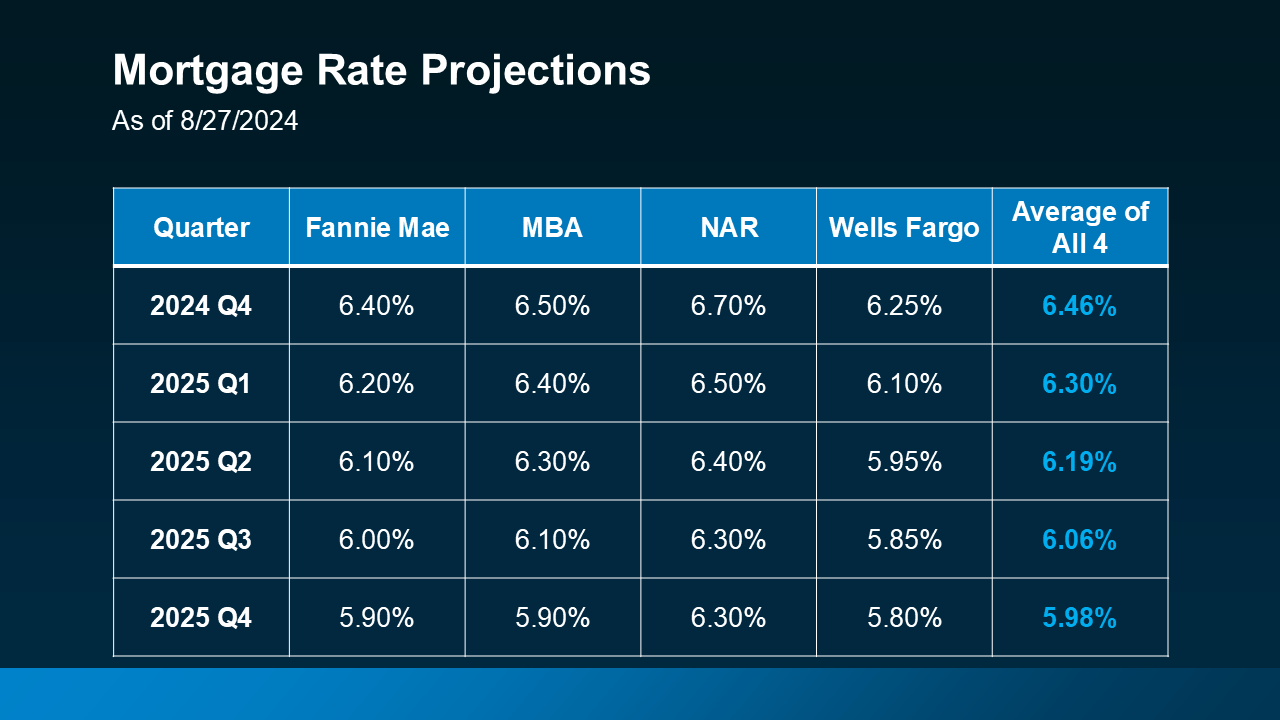

Mortgage rates play a significant role in the housing market. The forecasts for 2025 from Fannie Mae, the Mortgage Bankers Association (MBA), the National Association of Realtors (NAR), and Wells Fargo show an expected gradual decline in mortgage rates over the course of the next year (see chart below):

Mortgage rates are projected to come down because continued easing of inflation and a slight rise in unemployment rates are key signs of a strong but slowing economy. And many experts believe these signs will encourage the Federal Reserve to lower the Federal Funds Rate, which tends to lead to lower mortgage rates. As Morgan Stanley says:

“With the U.S. Federal Reserve widely expected to begin cutting its benchmark interest rate in 2024, mortgage rates could drop as well—at least slightly.”

The market will see an increase in both the supply of available homes on the market, as well as a rise in demand, as more buyers and sellers who have been sitting on the sidelines because of higher rates choose to make a move. That’s one big reason why experts are projecting an increase in home sales next year.

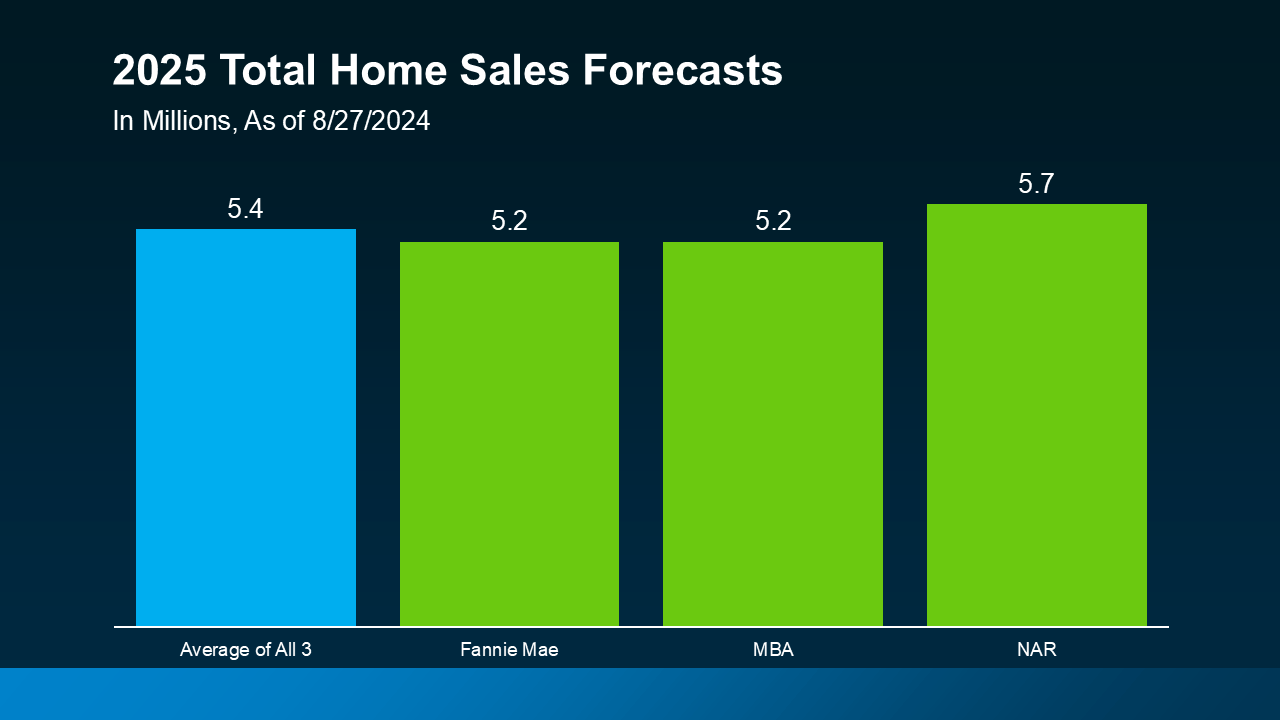

According to Fannie Mae, MBA, and NAR, total home sales are forecast to climb slightly, with an average of about 5.4 million homes expected to sell in 2025 (see graph below):

That would represent a modest uptick from the lower sales numbers in 2023 and 2024. For reference, about 4.8 million total homes were sold in 2023, and expectations are for around 4.5 million homes to sell this year.

While slightly lower mortgage rates are not expected to bring a flood of buyers and sellers back to the market, they certainly will get more people moving. That means more homes available for sale – and competition among buyers who want to purchase them.

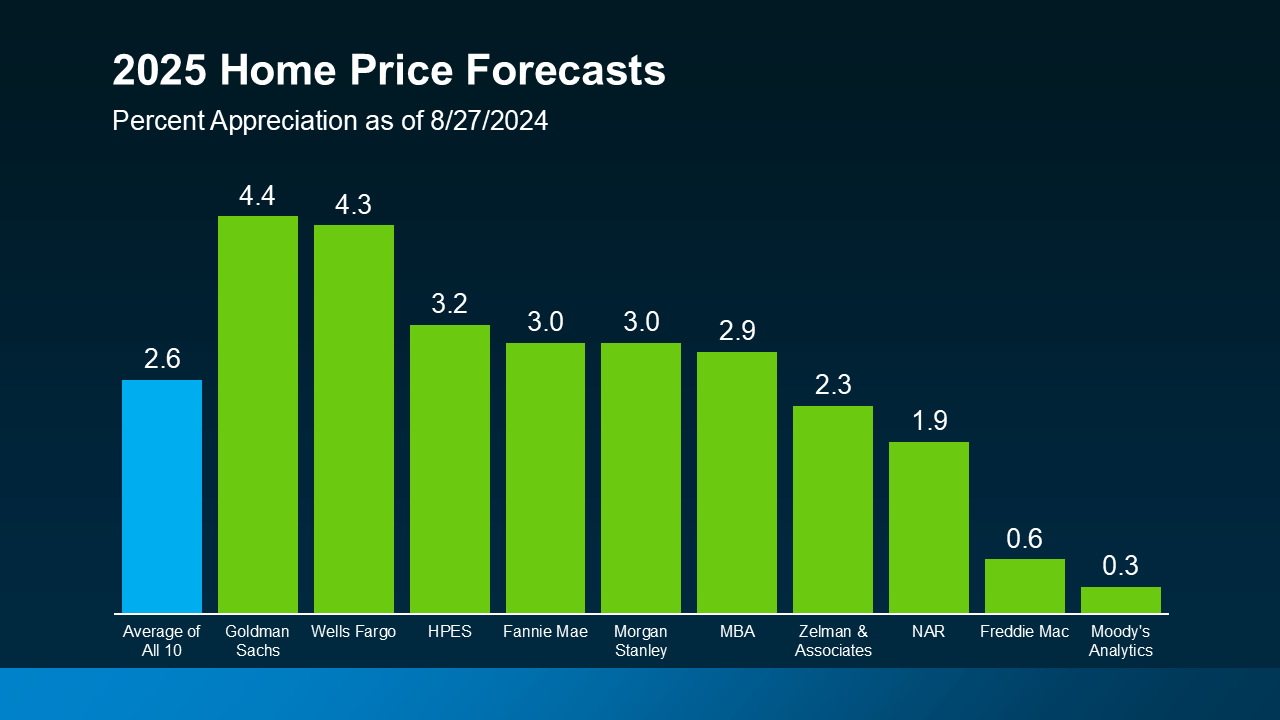

More buyers ready to jump into the market will put continued upward pressure on prices. Take a look at the latest price forecasts from 10 of the most trusted sources in real estate (see graph below):

On average, experts forecast home prices will rise nationally by about 2.6% next year. But as you can see, there’s a range of opinions on how much prices will climb. Experts agree, however, that home prices will continue to increase moderately next year at a slower, more normal rate. But keep in mind, prices will always vary by local market.

Understanding 2025 housing market forecasts can

help you plan your next move. Whether you're buying or selling, staying

informed about these trends will ensure you make the best decision

possible. Reach out to a trusted real estate agent to discuss how these

forecasts could impact your plans.

Article Courtesy of Keeping Current Matters /The KCM Blog

Here’s the good news that may surprise you: typically, Presidential elections have only had a small, temporary impact on the housing market. But your questions are definitely worth answering, so you don’t have to pause your plans in the meantime.

Here’s a look at decades of data that shows exactly what’s happened to home sales, prices, and mortgage rates in previous Presidential election cycles, so you can move forward with the facts as you weigh the pros and cons of your homeownership decision.

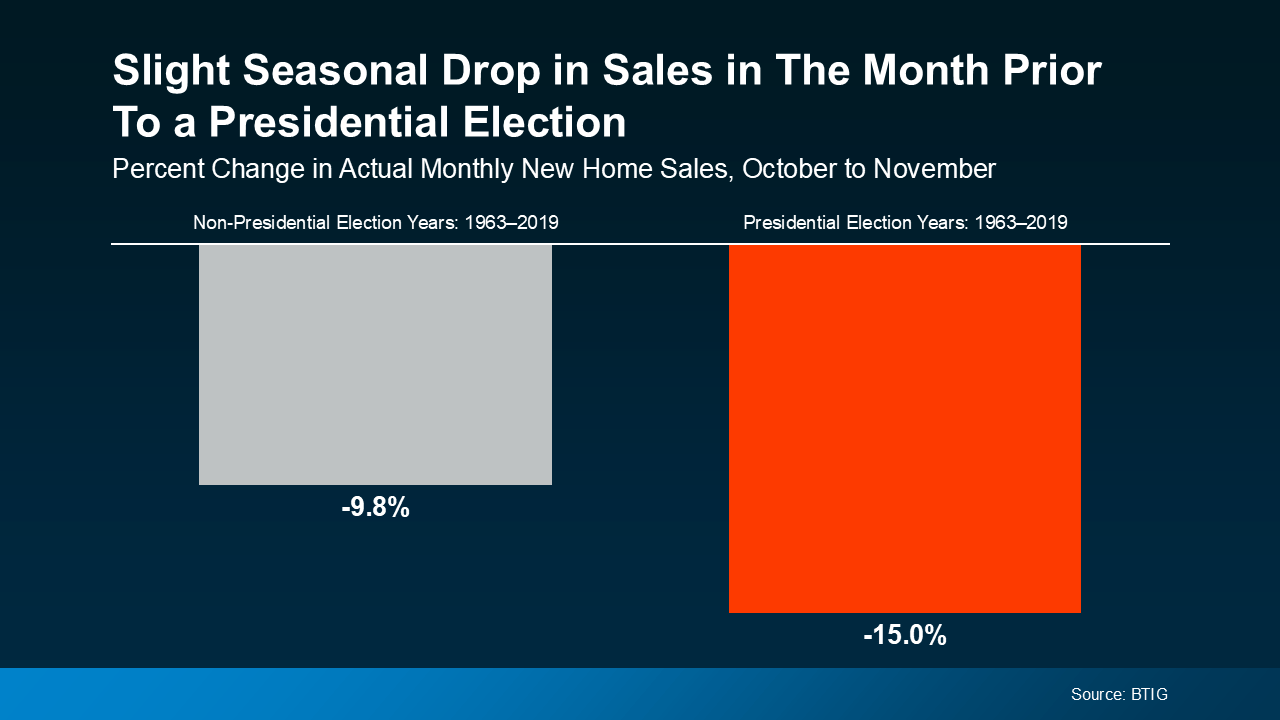

In the month leading up to a Presidential election, from October to November, there’s typically a slight slowdown in home sales (see graph below):

Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary.

Historically, home sales bounce right back and continue to rise the following year.

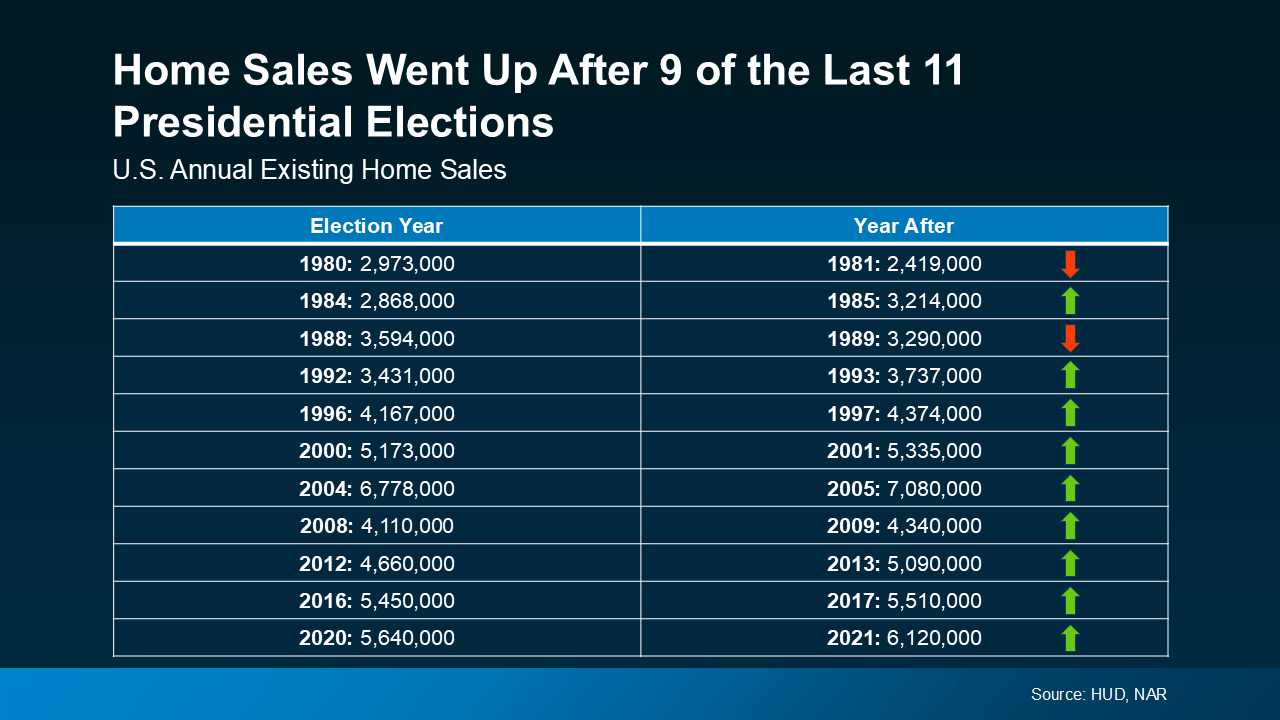

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after 9 of the last 11 Presidential elections, home sales went up the year after the election, and it’s been happening consistently since the early 1990s (see chart below):

You may also be wondering about home prices. Do prices come down during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist notes:

“An election year doesn’t alter the price trend that is already happening in the market.”

Home prices generally rise over time, regardless of an election cycle. So, based on what history shows, you can expect the current pricing trend in your local market to likely continue, barring any unusual market or economic circumstances.

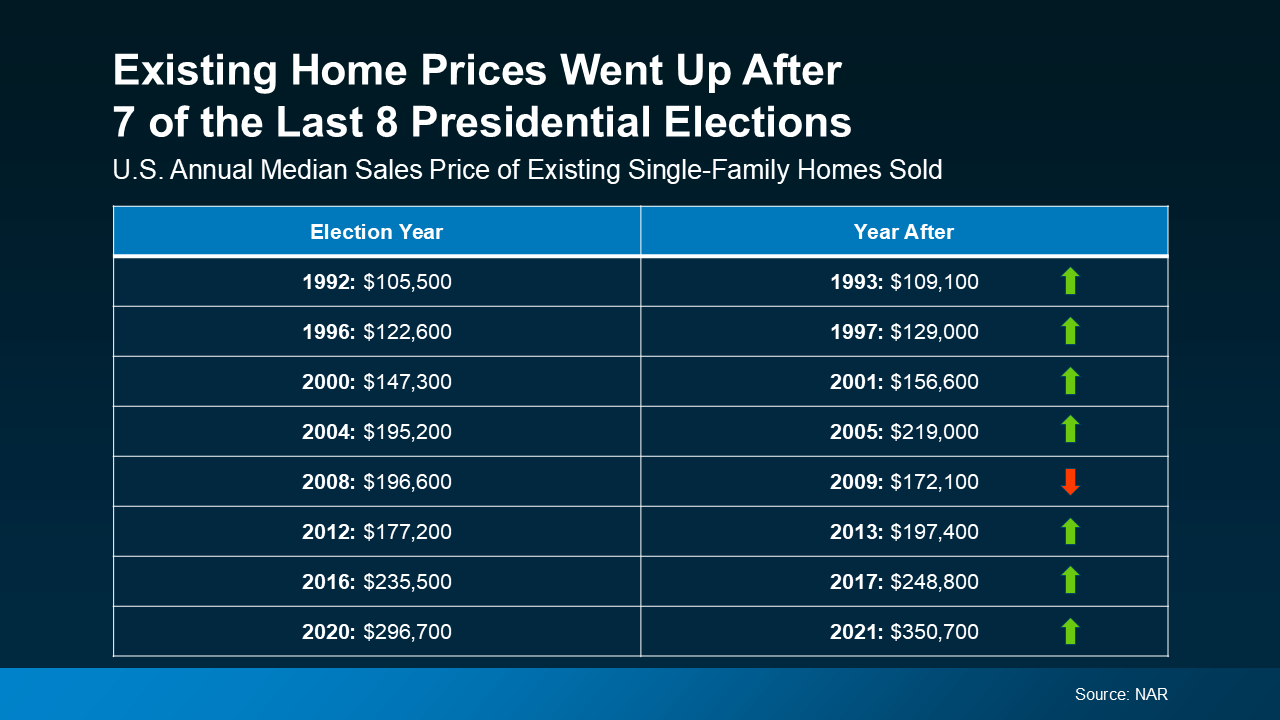

The latest data from NAR reveals that after 7 of the last 8 Presidential elections, home prices increased the following year (see chart below):

The one outlier was from 2008 to 2009, which was during the height of the housing market crash. That was certainly not a typical year. Today’s market, however, is much more resilient. And while prices are moderating nationally, they aren’t on an overall decline.

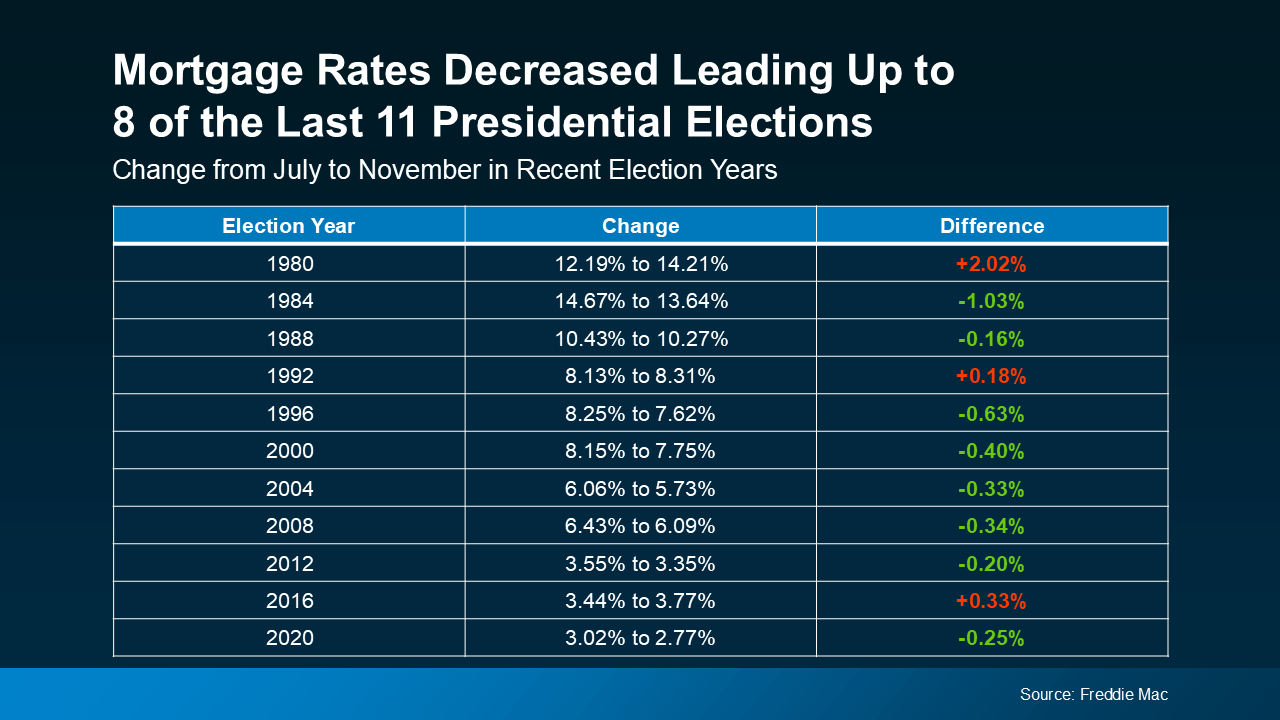

And the third thing that’s likely on your mind is mortgage rates, since they impact your monthly payment if you’re financing a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in 8 of them (see chart below):

And this year, we’ve already started to see that happen. Most experts also forecast mortgage rates will ease slightly throughout the rest of 2024. If that happens – and all signs right now indicate it should – this year will continue to follow the trend of declining rates. So, if you’re looking to buy a home in the coming months, this could be great news for your purchasing power.

What’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually minimal. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. And this means you don’t have to pause your plans in the meantime. For help navigating the market during this election cycle, reach out to a local real estate agent.

Article Courtesy of Keeping Current Matters/The KCM Blog

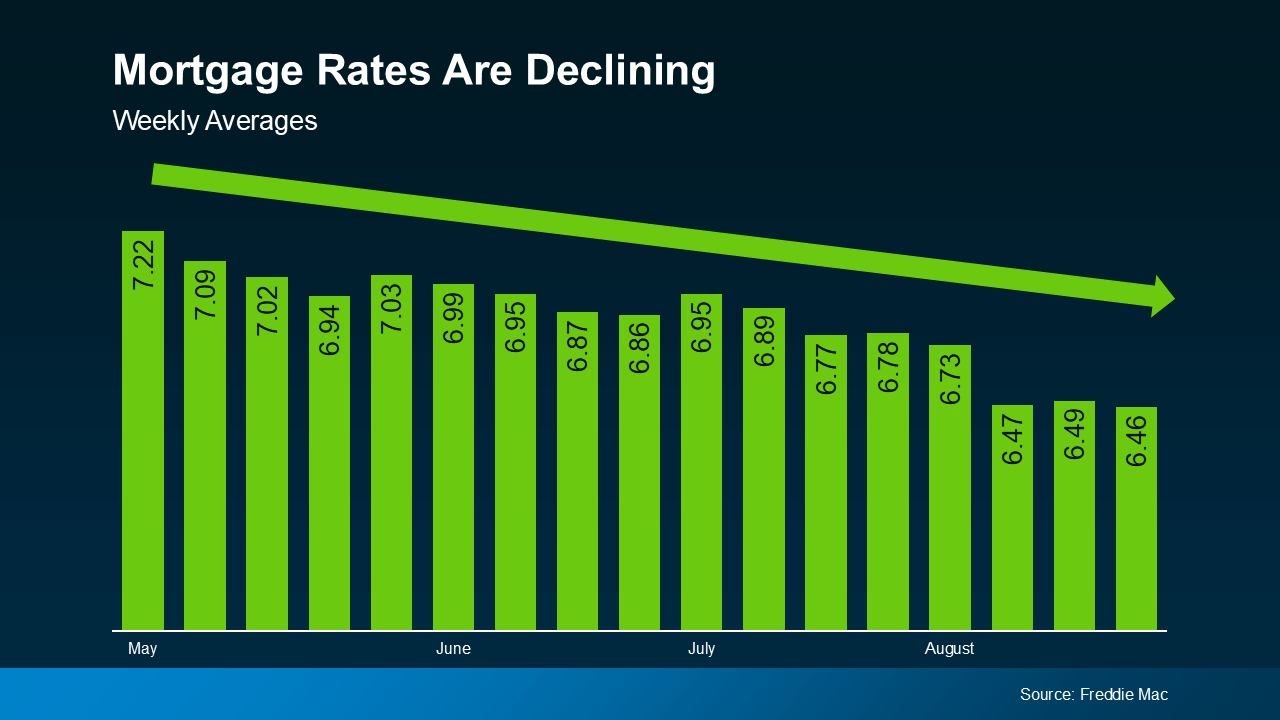

Experts say the overall downward trend should continue as long as inflation and the economy keeps cooling. But as new reports come out on those key indicators, there’s going to be some volatility here and there.

What you need to remember is it’s not wise to let those blips distract you from the larger trend. Rates are still down roughly a full percentage point from the recent peak compared to May.

And the general consensus is that rates in the low 6s are possible in the months ahead, it just depends on what happens with the economy and what the Federal Reserve decides to do moving forward.

Most experts are already starting to revise their 2024 mortgage rate forecasts to be more optimistic that lower rates are ahead. For example, Realtor.com says:

“Mortgage rates have been revised slightly lower as signals from the economy suggest that it will be appropriate for the Fed to begin to cut its Federal Funds rate in 2024. Our yearly mortgage rate average forecast is down to 6.7%, and we revised our year-end forecast to 6.3% from 6.5%.”

So, what does this mean for you and your plans to move? If you’ve been holding out and waiting for rates to come down, know that it’s already happening. You just have to decide, based on the expert projections and your own budget, when you’ll be willing to jump back in. As Sam Khater, Chief Economist at Freddie Mac, says:

“The decline in mortgage rates does increase prospective homebuyers’ purchasing power and should begin to pique their interest in making a move.”

As a next step, ask yourself this: what number do I want to see rates hit before I’m ready to move?

Maybe it’s 6.25%. Maybe it’s 6.0%. Or maybe it’s once they hit 5.99%. The exact percentage where you feel comfortable kicking off your search again is personal. Once you have that number in mind, you don’t need to follow rates yourself and wait for it to become a reality.

Instead, connect with a local real estate professional. They’ll help you stay up to date on what’s happening and have a conversation about when to make your move. And once rates hit your target, they’ll be the first to let you know.

If you’ve put your moving plans on hold because of higher mortgage rates, think about the number you want to see rates hit that would make you re-enter the market.

Once you have that number in mind, connect with a real estate professional so you have someone on your side to let you know when we get there.

Article Courtesy of Keeping Current Matters / The KCM Blog

And if you aren’t working with an agent, you may not realize that. Here’s the downside. If you’re not informed, you can’t adjust your strategy or expectations to today’s market. And that can lead to a number of costly mistakes.

Here’s a look at some of the most common ones – and how an agent will help you avoid them when you sell.

Many sellers set their asking price too high and that’s why there’s an uptick in homes with price reductions today. An unrealistic price will deter potential buyers, cause an appraisal issue, or lead to your house sitting on the market longer. An article from the National Association of Realtors (NAR) explains:

“Some sellers are pricing their homes higher than ever just because they can, but this may drive away serious buyers and result in unapproved appraisals . . .”

To avoid falling into this trap, partner with a pro. An agent uses recent sales of similar homes, the condition of your house, local market trends, and so much more to find the price that’ll attract more buyers and open the door for multiple offers and a faster sale.

You may try to skip important repairs, thinking you can pass the task on to your buyer. But visible issues (even if they’re small) can turn off potential buyers and result in lower offers or demands for concessions. As Money Talks News says:

“Home shoppers like to turn on lights, flush toilets and run the water. If these basic things don’t work, they may assume you’ve skipped other maintenance. Homes that appear neglected aren’t likely to fetch top price.”

If you want to get your house ready to sell, the best place to turn to for advice is your agent. They’ll be able to do a walk-through with you and point out anything you’ll need to tackle before the photographer comes in.

Buyers today are feeling the pinch of high home prices and mortgage rates. With affordability that tight, they may come in with an offer that’s lower than you’d want to see – especially if you didn’t stage, price, or market the house well.

It’s important you don’t take this personally. Getting overly emotional can put the sale at risk. As an article from Ramsey Solutions says:

“Remember, a buyer’s offer is not a reflection of their opinion of your home or your housekeeping abilities. . . The sale of your home is strictly a business transaction. If they start out with a low offer, don’t take it personally and get emotional. Instead, channel that energy toward negotiating. Work with your agent and make a counteroffer.”

The supply of homes for sale has grown. That means buyers have more options, and with that comes more negotiation power. As a seller, you may see more buyers getting an inspection, requesting repairs, or asking for help with closing costs today. You need to be prepared to have those conversations. As U.S. News Real Estate explains:

“If you’ve received an offer for your house that isn’t quite what you’d hoped it would be, expect to negotiate . . . the only way to come to a successful deal is to make sure the buyer also feels like he or she benefits . . . consider offering to cover some of the buyer’s closing costs or agree to a credit for a minor repair the inspector found.”

An agent will walk you through what levers you may want to pull based on your own goals, budget, and timeframe.

Notice anything? For each of these mistakes, partnering with an agent helps prevent them from happening in the first place. That makes trying to sell your house without an agent’s help the biggest mistake of all.

Real estate agents have experience and expertise in pricing, marketing, negotiating, and more. That knowledge streamlines the selling process and usually results in drumming up more interest and ultimately can get you a higher final price.

If you want to avoid making mistakes like these, you need to work with a real estate agent.

{kind=link}

{kind=link}